There’s a version of the self-driving car story that’s been running for fifteen years: perpetually five years away, always promising, never quite arriving. That version is finally becoming outdated.

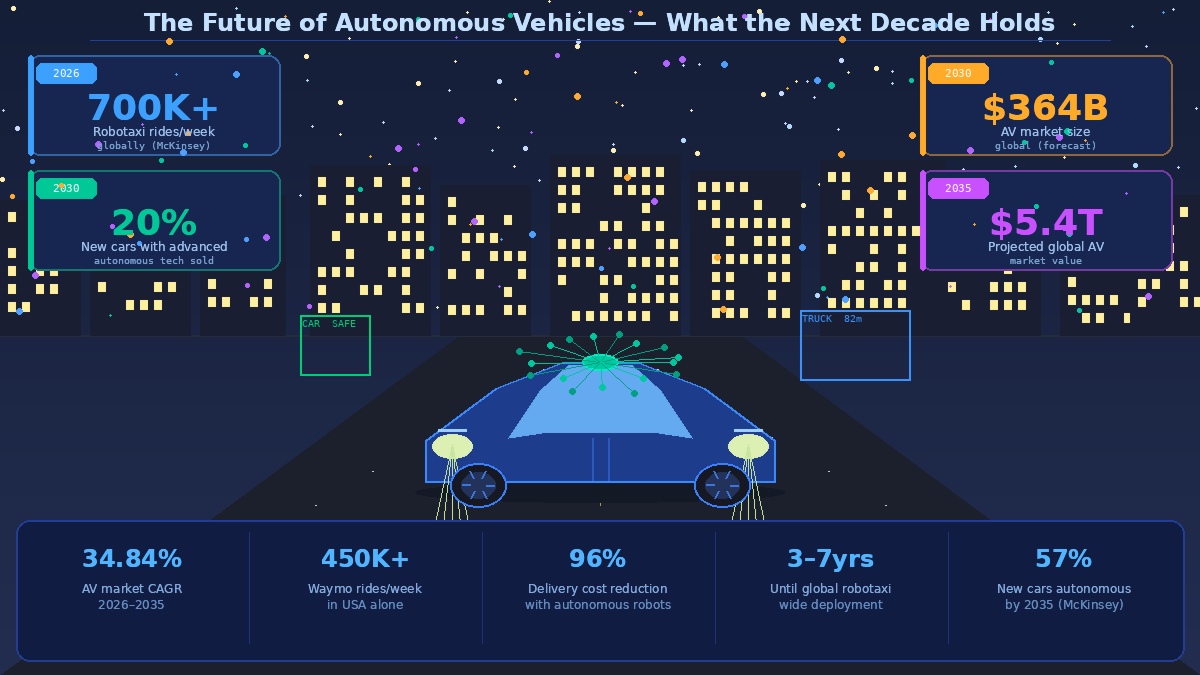

In early 2026, McKinsey reported that over 700,000 fully autonomous robotaxi rides are now completing every week globally — more than 450,000 of those in the United States alone. Aurora launched the first fully autonomous long-haul commercial freight runs between Dallas and Houston in April 2025. Waymo expanded its driverless service to Atlanta in summer 2025 and has since added Miami to its roadmap. The technology hasn’t arrived all at once, and it hasn’t arrived everywhere — but it has arrived.

The global autonomous vehicle market was valued at $273.75 billion in 2025 and is forecast to grow at 34.84% compound annual growth rate through 2035, reaching a projected $5.4 trillion. These aren’t speculative numbers from early-stage startups. They reflect a market that has crossed a critical threshold from R&D to commercial deployment.

Where the Industry Actually Stands in 2026

The most important distinction to understand is that “autonomous vehicles” isn’t one category — it’s a spectrum. Over 55% of all newly manufactured vehicles globally now include Level 2 capabilities: adaptive cruise control, lane-keeping, automatic emergency braking. These are not self-driving systems. They’re driver assistance features that reduce fatigue and prevent certain types of collisions.

Level 3 is where things get genuinely interesting. The L3 segment holds 46% of the autonomous vehicle market in 2025. An L3 system can manage the car in defined conditions — highway driving, stop-and-go traffic — without the driver actively controlling it, though the driver must remain available to take over. Honda’s 0 Series launched its L3 system in 2026. Mercedes-Benz’s Drive Pilot L3 system, operating at speeds up to 130 km/h on approved German motorways, uses a distinctive turquoise roof light to signal autonomous operation to other drivers.

Level 4 — fully driverless within a geofenced operational area — is where Waymo, Baidu’s Apollo Go, and WeRide are currently operating commercially. These vehicles require no human backup driver within their defined service areas. Waymo’s fleet has now logged over 160 million fully driverless kilometres. WeRide and Renault ran a public trial of an autonomous Level 4 Robobus in Barcelona in March 2025.

Level 5 — fully autonomous in any condition, anywhere in the world — does not commercially exist yet, and most honest forecasts don’t see it arriving this decade.

The Regional Race: US, China, and Everyone Else

The United States and China are leading the world in autonomous vehicle deployment, and the gap to everywhere else is significant. McKinsey’s January 2026 industry survey found that most experts expect a dedicated Chinese technology stack — driven by separate supply chains, independent chip manufacturers like Horizon Robotics (which holds 49% of China’s autonomous chip market), and strong government support for smart city infrastructure.

China has over 250,000 commercial autonomous rides per week and is advancing rapidly on both consumer vehicles and logistics applications. By 2030, over 80% of vehicles in China are expected to include advanced driver assistance systems. In North America, state-level testing permits in California and Arizona have created the world’s most permissive environment for autonomous vehicle development.

Europe is moving more carefully. The UK pushed back its expected approval date for fully self-driving cars to the second half of 2027. The EU is pursuing regulatory harmonisation rather than racing to deployment, which has made it an observer in the current wave of commercial rollouts rather than a participant.

Autonomous Trucks and Last-Mile Delivery

The consumer robotaxi gets most of the coverage, but autonomous freight may generate more economic value in the near term. Aurora’s commercial autonomous trucking service launched in April 2025 on the Dallas-Houston corridor — a high-volume, well-mapped freight route where the technology’s current constraints are easiest to manage.

The autonomous last-mile delivery market is projected to grow from $28.5 billion in 2025 to $163.45 billion by 2033 — a 24.4% compound annual growth rate. Delivery robots from Starship and Amazon Scout are already operating in defined urban zones, and Gartner projects over one million drones delivering retail goods by 2026. The economics are compelling: autonomous robots can cut delivery costs by up to 96%, from around $1.60 per delivery to $0.06.

The Technology Pushing Everything Forward

Two developments are accelerating the timeline more than anything else. The first is computing power. Modern autonomous vehicles run on platforms delivering 500–2,000 trillion operations per second — NVIDIA’s Drive Thor platform reaches 2,000 TOPS, enabling millisecond-level detection, prediction, and path planning that Level 3–4 systems require. The second is next-generation LiDAR, which now detects objects beyond 1,000 metres, giving vehicles significantly more reaction time at highway speeds. The automotive LiDAR market is growing at 41.6% annually, projected to reach $9.59 billion by 2030.

Both Tesla and Waymo have also converged on end-to-end AI architectures — training foundation models on vast amounts of real-world driving data rather than building rule-based modular systems. The debate over camera-only versus sensor-fusion approaches continues, but the underlying AI methodology is becoming similar.

What Does 2035 Actually Look Like?

McKinsey’s industry consensus points to 20% of new passenger cars sold globally including advanced autonomous driving technology by 2030, rising to 57% by 2035. Robotaxis will be widely commercially available in major cities within three to seven years, according to surveyed industry leaders.

What won’t happen is a sudden switch where every car on every road drives itself overnight. The transition will be gradual, geographically uneven, and shaped as much by regulation and infrastructure as by technology. The cities and countries that invest in smart road infrastructure, clear legal frameworks for Level 4 operation, and public education about how these systems work will see autonomous vehicles far sooner than those that don’t.

The future of autonomous vehicles isn’t a single arrival date. It’s already happening, one city and one corridor at a time.