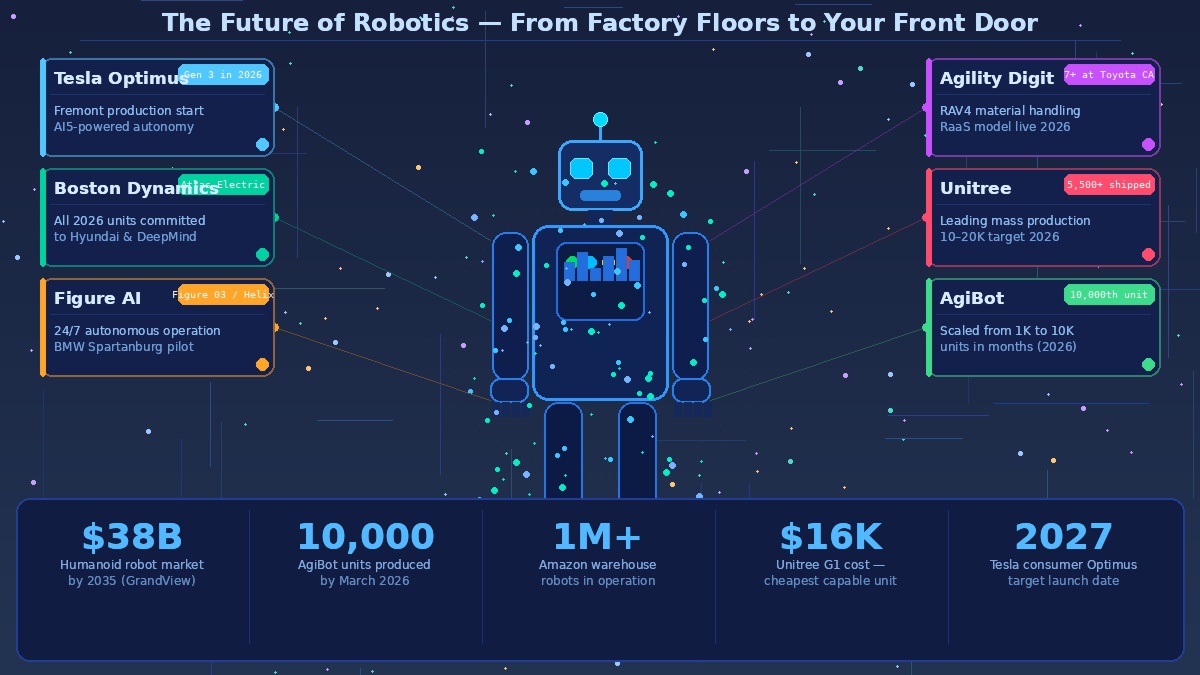

Something shifted in early 2026. It’s not that humanoid robots suddenly became capable — that’s been a gradual process playing out for years. It’s that they started shipping. AgiBot produced its 10,000th humanoid robot in late March 2026, scaling from 1,000 units in 2025 to 10,000 within months. Unitree shipped more than 5,500 robots in 2025 alone and is targeting 10,000 to 20,000 in 2026. Boston Dynamics’ electric Atlas has entered commercial production with its entire 2026 allocation already committed to Hyundai and Google DeepMind. The era of robotics as a lab experiment is closing. The era of robotics as an industry is opening.

McKinsey’s April 2026 report put it plainly: the robotics supply chain is the most underappreciated constraint on humanoid scale, and for companies that move now, it is the most significant opportunity in a generation.

What Humanoid Robots Are Actually Doing Right Now

The gap between robotics marketing and robotics reality is narrowing fast, but it’s still worth being clear about what’s actually happening versus what’s been announced.

Agility Robotics’ Digit is the furthest along in real-world commercial deployment. In February 2026, Agility signed a Robots-as-a-Service agreement with Toyota Motor Manufacturing Canada, and seven Digit units are now actively handling RAV4 material logistics at the Woodstock plant. This isn’t a demonstration — it’s a live commercial operation with a subscription pricing model. Figure AI’s Figure 03 demonstrated continuous unsupervised operation at BMW’s Spartanburg facility, and the company is scaling production with a target of running robot-built-robot production lines within 24 months.

At the same time, NVIDIA’s Jensen Huang — who made the most memorable image of the robotics wave, photographed flanked by eight humanoid systems at GTC 2024 — continues to position NVIDIA as the computing infrastructure for the entire sector. Its GR00T N1 and N1.5 foundation models, released in 2025, are the first open, customisable humanoid AI models pairing a vision-language reasoning backbone with a diffusion transformer for motor control. Adding synthetic motion data through NVIDIA’s GR00T-Dreams simulation pipeline improved task success rates by approximately 40% compared to real-world data alone.

The Three Architectures Competing for the Future

The robotics industry in 2026 isn’t one monolithic approach — it’s three distinct bets on what the future looks like.

General-purpose humanoids. Tesla’s Optimus, Figure’s robots, and Boston Dynamics’ Atlas are all pursuing the same vision: a robot shaped like a human that can do any physical task a human can do, in any environment humans inhabit. The appeal is obvious — human environments are designed for human bodies, so a human-shaped robot can operate in them without redesigning the world. The challenge is equally obvious: general capability is extraordinarily hard to achieve and the power and dexterity requirements are demanding. Current humanoid batteries give two to four hours of active operation. Solid-state batteries, still not in mass production for robotics, promise six to eight hours — a threshold that would change the economics dramatically.

Specialised industrial robots. The more pragmatic approach is to build robots optimised for specific, well-defined tasks in controlled environments. Amazon now has over one million robots operating across its warehouses — none of them humanoid, all of them extremely effective at what they do. This segment is already profitable and scaling fast.

Foundation model-powered adaptability. Google DeepMind’s Gemini Robotics family, built on Gemini 2.0, can generate robot control code on the fly and run that model locally on the robot itself — a critical development for real-world deployment where cloud connectivity isn’t always reliable. A robot receiving an instruction in plain English, interpreting its environment, and executing a response without being pre-programmed for that specific scenario is what Vision-Language-Action models are enabling. This is the architecture most researchers believe will define the next generation.

The China Factor

China’s role in the robotics race deserves specific attention. The 2025 Robot Olympics in Beijing — a dedicated competition for humanoid capabilities — signals how seriously China is treating this as a national priority. AgiBot’s production scale-up, Unitree’s aggressive shipping numbers, and the emergence of multiple Chinese humanoid startups reflect both substantial government support and the severe labour shortage pressures that make automation economically urgent.

Unitree’s G1 is the most striking example of China’s cost advantage: a capable bipedal robot available for approximately $16,000 — a fraction of Western equivalents. China is likely to dominate the mid-market robotics segment globally for the same reason it dominates consumer electronics: manufacturing scale, supply chain control, and competitive pricing.

What’s Still Hard — And Why It Matters

Dexterous manipulation remains the most significant unsolved problem. Most humanoid robots can pick up and place objects with reasonable reliability. Very few can handle fragile items, operate tools with precision, thread a needle, or perform the kind of fine motor work that humans do constantly without thinking. The gap between “can move boxes” and “can replace a human on a general-purpose factory line” is still substantial.

Reliability in unstructured environments is the other major challenge. Robots perform well in mapped, known environments. Kitchens, homes, hospitals — environments with clutter, variability, and unpredictability — remain difficult. Tesla is targeting consumer Optimus availability by late 2027, and Elon Musk said in January 2026 that he expects the robot to eventually sell for less than $20,000. That timeline and price point would represent a genuine step change. Whether it arrives on schedule is a different question.

The Decade Ahead

The robotics market is projected to reach $38 billion by 2035. The more significant number is the labour it displaces and augments. The World Economic Forum’s scenarios for the 2030s include humanoid robots handling a majority of routine physical labour in manufacturing and logistics in developed economies, with the human workforce shifting toward supervisory, creative, and interpersonal roles.

That transition is not painless or evenly distributed. But the direction is clear. The robots aren’t coming. They’re shipping.