The autonomous vehicle industry has a brutal reputation. Cruise, Argo AI, TuSimple, and Starsky Robotics collectively raised $12.6 billion before shutting down. Ghost Autonomy raised $219 million with backing from OpenAI’s Startup Fund and still closed its doors. This is a sector where deep pockets and brilliant engineering are not enough to guarantee survival.

And yet, in 2026, the survivors are thriving like never before. The autonomous vehicle market has attracted more than $65 billion in cumulative startup funding, making it one of the most capital-intensive technology sectors of the past decade. Waymo’s $16 billion February 2026 round alone exceeds the total lifetime fundraising of every other AV startup combined — a sign of extraordinary capital concentration at the top.

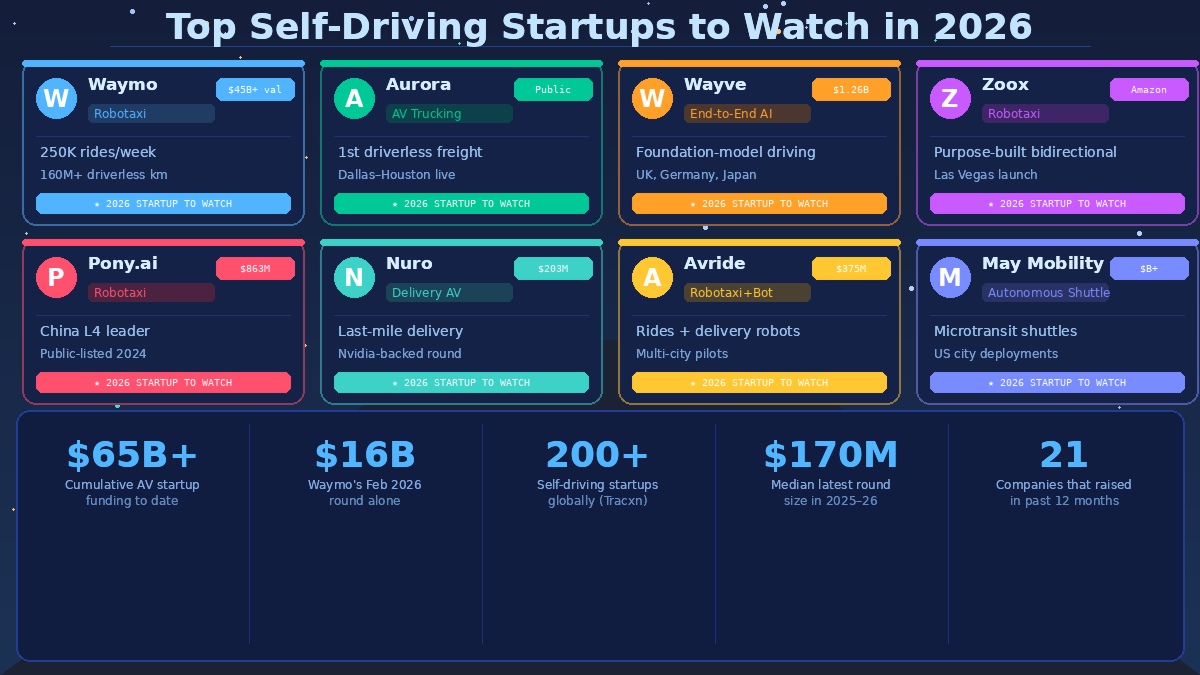

Here are the companies that have made it through the cull and are defining what comes next.

Waymo — The Undisputed Leader

It started as a Google project in 2009 and has become the most valuable and operationally mature autonomous vehicle company in the world. Waymo is completing over 250,000 paid rides per week across San Francisco, Los Angeles, Phoenix, and Austin, with a fleet exceeding 1,500 vehicles that it plans to double to 3,500 in 2026. It has logged more than 160 million fully driverless kilometres. Its February 2026 funding round of $16 billion is the largest in the sector’s history. Waymo is no longer a startup in the traditional sense — it’s the benchmark every other company is measured against. Expansion to Tokyo, London, Miami, and more than a dozen other cities is planned for 2026.

Aurora — Driverless Trucking at Commercial Scale

Aurora did something no other company had achieved: it launched the world’s first commercial driverless freight service, running fully autonomous trucks on the Dallas-Houston corridor starting in May 2025. Now publicly listed, Aurora is focused on the freight market, where the economics of autonomy are arguably more compelling than robotaxis. Highway trucking is a more constrained, repeatable problem than chaotic urban driving, and the driver shortage in long-haul freight makes the business case urgent. Aurora is scaling its driverless lanes across Texas and beyond.

Wayve — The End-to-End AI Bet

Wayve, based in the UK, has taken a fundamentally different technical approach than most competitors. Rather than building heavily mapped, sensor-laden systems, it uses an end-to-end AI foundation model trained to drive the way a human learns — through experience and generalisation rather than pre-programmed rules. Backed by Microsoft, SoftBank, and Nvidia, it raised $1.26 billion and is partnered with Uber and Nissan. Wayve is testing in the UK, Germany, and Japan, and its approach — if it scales — could prove far more transferable across cities than map-dependent rivals. It represents the most credible European challenger in the sector.

Zoox — Amazon’s Purpose-Built Robotaxi

Owned by Amazon, Zoox isn’t retrofitting existing cars — it designed a purpose-built, bidirectional robotaxi from scratch, with no steering wheel and the ability to drive in either direction. It launched its public robotaxi service in Las Vegas in September 2025 and is building a serial production facility to scale manufacturing. With Amazon’s resources behind it and a genuinely novel vehicle design, Zoox is one of the few companies positioned to challenge Waymo’s operational lead in the robotaxi space.

Pony.ai — China’s Robotaxi Frontrunner

Pony.ai is among the leaders in China’s rapidly advancing autonomous vehicle market. Now publicly listed, with $863 million raised in its most recent activity, it operates Level 4 robotaxi services across major Chinese cities. China’s regulatory environment and government support for autonomous driving have allowed companies like Pony.ai to scale quickly, and the country is positioned to be a dominant force in global AV deployment. For investors and observers watching where the technology will scale fastest, Pony.ai is essential to understand.

Nuro — Delivery, Not Passengers

Nuro took a smart strategic decision early: rather than competing in the crowded, high-stakes robotaxi market, it focused on autonomous delivery. Its small, purpose-built vehicles carry goods rather than people, which dramatically lowers the safety stakes and regulatory complexity. Nuro has partnered with major brands including Walmart and Chipotle, and recently closed a $203 million round with Nvidia joining as an investor. Autonomous delivery vans have shown the strongest capital efficiency of any AV category, and Nuro is the clearest pure-play bet on that thesis.

Avride — Rides and Robots Combined

Avride is pursuing both autonomous ride-hailing and delivery robots simultaneously, raising $375 million to fund multi-city pilots. The dual approach hedges across two of the most promising AV applications, and the company’s delivery robot technology shares significant overlap with its passenger vehicle stack. It’s one of the more interesting diversified plays in a market where most companies are betting everything on a single application.

May Mobility — Microtransit and Shuttles

May Mobility focuses on autonomous shuttles and microtransit — fixed-route and on-demand transport in defined service areas like campuses, downtowns, and suburban communities. This is a less glamorous corner of the AV world but a genuinely practical one: shuttles operating predictable routes at lower speeds are an easier autonomy problem than open robotaxi service, and the public transit applications address real mobility gaps. May Mobility has steadily expanded across US cities and represents the pragmatic end of the autonomous spectrum.

What the Funding Tells Us

The market in 2026 is narrow rather than broad. Only 21 unique companies produced disclosed equity rounds over the past 12 months, and the median round size has risen to roughly $170 million — a significant jump from pre-2023 norms. This signals a maturing industry where capital is concentrating in proven players rather than spreading across speculative bets.

Public-road ride-hailing is the thesis investors are most willing to fund at scale, which is why Waymo, Wayve, Pony.ai, and Avride are attracting the largest rounds. The era of funding any startup with an autonomous driving pitch is over. What’s left are the companies that have demonstrated real technology, real deployments, and a credible path to profitability.

The graveyard of failed AV startups is a reminder that this is one of the hardest problems in technology. But the survivors on this list have crossed from promise to product — and they’re the ones who will shape how the world moves over the next decade.